Welcome to a comprehensive exploration of captive insurance, an innovative and powerful solution in the world of risk management. Captive insurance has gained considerable traction in recent years, offering businesses an alternative risk financing approach that allows them to take control of their insurance needs. At its core, captive insurance involves the creation of a dedicated insurance company to cover the risks of its parent organization or a group of related entities. This unique vehicle provides an opportunity for businesses to tailor their insurance coverage, manage their risks more effectively, and potentially enjoy financial benefits along the way.

One of the key aspects of captive insurance can be found in the Internal Revenue Code section 831(b), commonly referred to as the "831(b) tax code." This specific provision enables qualifying insurance companies, known as microcaptives, to operate under a more favorable tax regime. Essentially, it allows these captive insurance companies to be taxed only on their investment income and not on their underwriting profits, provided that certain criteria are met as per the IRS guidelines.

The utilization of captive insurance can be a strategically prudent move for businesses across various industries, as it offers opportunities for enhanced efficiency and flexibility. By establishing their own captive insurance company, organizations can potentially streamline operations, gain better control over claim management, and minimize exposure to volatile commercial insurance markets. Additionally, the captives can be customized to closely align with the specific risk profile, offering tailored coverage while potentially reducing overall insurance costs.

In the pages that follow, we will delve deeper into the intricacies of captive insurance, exploring the benefits and challenges associated with this unchained solution. We will examine the eligibility criteria for microcaptives under the 831(b) tax code, unravel the tax implications, and offer insights into the regulatory landscape surrounding captive insurance. Join us on this educational journey as we unlock the potential of captive insurance and gain a deeper understanding of its strategic value.

Section 1: An Introduction to 831b

Captive insurance, specifically the 831(b) tax code enacted by the IRS, has gained significant attention in recent years. This innovative solution offers businesses an alternative approach to managing risks and protecting their assets. Let’s delve into what 831b is all about.

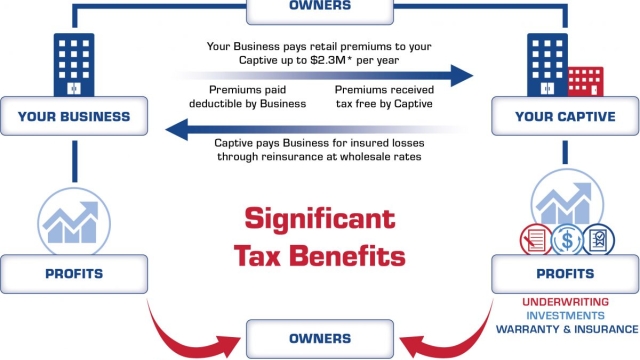

Captive insurance, in simple terms, involves a business creating its own insurance company to cover its risks. The 831(b) tax code refers to a specific provision that allows these captive insurance companies to enjoy certain tax advantages. Under this provision, eligible small insurance companies with annual written premiums of $2.3 million or less can elect to be taxed only on their investment income. This means they are exempt from paying taxes on premiums received, keeping a larger portion of their income for potential claims or investments.

The IRS 831(b) tax code has been a game-changer for many small to mid-size businesses looking to optimize their risk management strategies. By forming a captive insurance company and taking advantage of these tax benefits, businesses can effectively control their insurance costs, customize coverage, and mitigate risk in a more tailored manner.

Overall, the 831(b) tax code provides businesses with a powerful tool to enhance their financial stability, as well as gain more control and flexibility over their insurance programs. In the next sections, we will further explore captive insurance and explore the practical implications of incorporating it into a business strategy.

Section 2: The Concept of Captive Insurance

Captive insurance is an innovative risk management strategy that has gained significant attention in recent years. This concept revolves around the creation of a specialized insurance company, known as a captive insurer, to provide coverage for the risks faced by its parent company or group of related entities.

These captive insurers operate under a unique set of rules and regulations outlined in the Internal Revenue Service (IRS) tax code section 831(b). This particular section allows captive insurers to be taxed only on their investment income, provided that their annual premiums do not exceed $2.3 million. Captive insurance companies that qualify under this tax code are often referred to as microcaptives.

By forming a captive insurer, businesses can gain more control over their insurance programs, tailor coverage to their specific needs, and potentially reduce costs. Instead of relying solely on traditional commercial insurers, companies can establish their own captive insurer to underwrite risks that are not adequately covered in the commercial market.

Captive insurance not only brings financial advantages but also promotes a proactive risk management culture. By assuming the risks through their captive insurer, businesses can effectively identify, mitigate, and manage their unique risks, leading to improved risk management practices in the long run.

Overall, the concept of captive insurance presents businesses with an alternative risk-financing tool that can increase flexibility, improve risk management, and potentially provide cost savings. Understanding the fundamentals of captive insurance is essential for businesses looking to explore this innovative solution and make informed decisions regarding their insurance needs.

Section 3: Navigating the IRS 831b Tax Code

The IRS 831b tax code is a critical aspect to consider when exploring captive insurance solutions. Understanding the intricacies of this code is essential to ensure compliance and maximize the benefits of opting for a captive insurance arrangement.

One of the primary advantages of the IRS 831b tax code is that it allows eligible captive insurance companies to receive favorable tax treatment. Under this code, captive insurance companies with annual written premiums of $2.3 million or less can elect to be taxed only on their investment income. This distinction can result in substantial tax savings for businesses that meet the outlined criteria.

However, it is important to note that while the IRS 831b tax code offers appealing opportunities, it also comes with certain restrictions. Captive insurance companies opting for this tax treatment must adhere to specific guidelines set forth by the IRS. It is crucial to ensure compliance with these guidelines to avoid any unwanted scrutiny or potential penalties.

Microcaptives, a term often used to describe captive insurance companies that fall under the IRS 831b tax code, have gained popularity in recent years. These microcaptives provide an alternative risk management solution for small to mid-sized businesses, allowing them to effectively manage their risks while potentially reducing their overall insurance costs.

In summary, the IRS 831b tax code plays a significant role in the captive insurance landscape. By understanding its requirements and limitations, businesses can leverage this code to create tailored insurance solutions that align with their unique needs and objectives. It remains crucial to consult with experienced professionals who can navigate the complexities of this tax code and ensure compliance for a successful captive insurance endeavor.