Are you tired of being tied down by traditional insurance coverage? Looking for a way to take control of your insurance needs and potentially save money at the same time? Well, look no further than captive insurance. Captive insurance is a unique and powerful alternative to traditional coverage that allows businesses to tailor their insurance solutions to their specific needs.

At the heart of captive insurance is the concept of 831(b), a tax code provision that enables businesses to form their own insurance company, commonly known as a microcaptive. This innovative approach allows companies to retain more control over their risk management processes and potentially reduce their insurance costs. By creating their own insurance entity, businesses can design customized policies, effectively managing their exposure to risks that may not be adequately addressed by traditional insurance providers.

With captive insurance, businesses can break free from the limitations of standardized coverage and pave their own path towards a more efficient and cost-effective risk management strategy. By taking advantage of the flexibility offered by captive insurance, companies can align their coverage with their unique risk profiles, ensuring that they are adequately protected while minimizing unnecessary expenses.

In this article, we will explore the ins and outs of captive insurance, demystifying the complexities surrounding the IRS 831(b) tax code and shedding light on the benefits and potential pitfalls of implementing a captive insurance program. Whether you’re a small business owner seeking greater control over your insurance costs or a risk management professional looking to delve into the world of captive insurance, this article will serve as your comprehensive guide to unleashing the power of captive insurance and reaping the rewards it has to offer. So, let’s dive in and discover the untapped potential of this game-changing insurance solution.

Understanding Captive Insurance

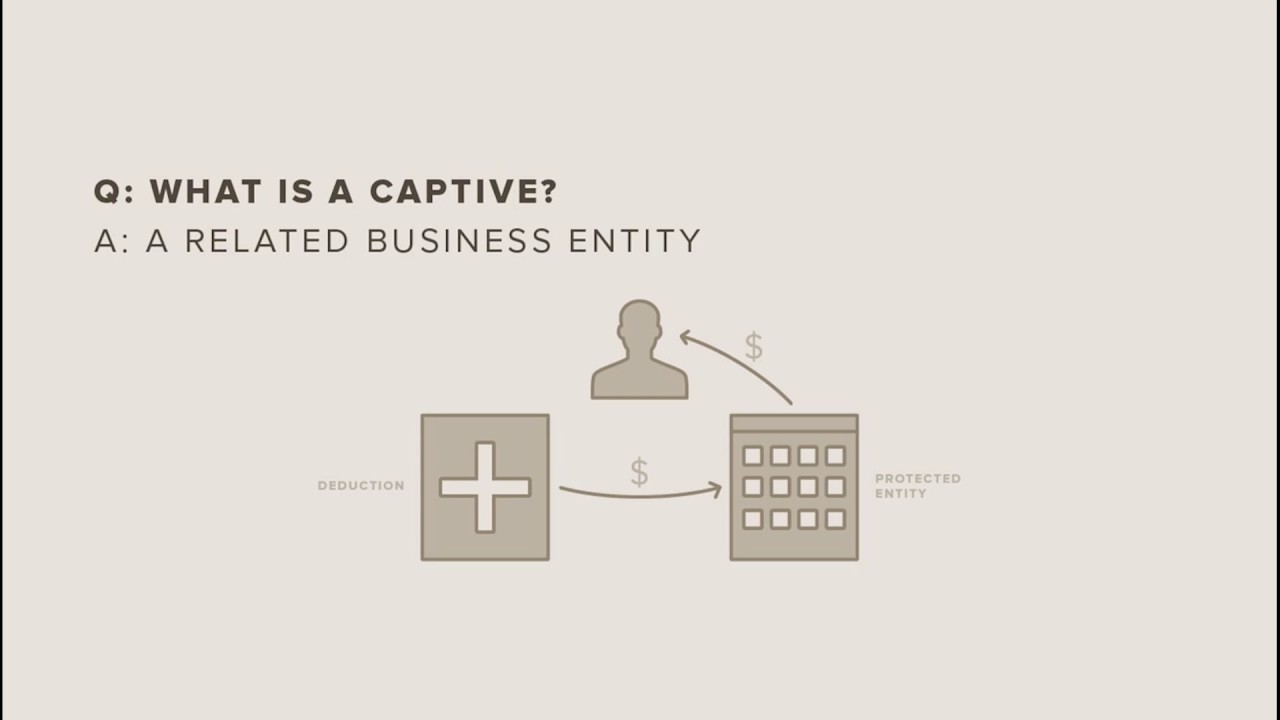

Captive insurance, also known as microcaptive insurance, is a unique and powerful alternative to traditional coverage options. It operates under the IRS 831(b) tax code, which provides certain tax advantages for small insurance companies.

Unlike purchasing insurance from traditional carriers, captive insurance allows businesses to create their own insurance company to cover their specific risks. By forming a captive insurance company, businesses can gain more control over their coverage and potentially reduce costs.

Under the IRS 831(b) tax code, captive insurance companies that have annual premiums under a certain threshold can enjoy tax benefits. These tax advantages can include lower tax rates and the ability to accumulate wealth within the captive to be used for future claims.

Overall, captive insurance offers businesses the opportunity to break free from the limitations of traditional coverage and tailor their insurance solutions to their unique needs. By understanding the concept of captive insurance and its potential benefits, businesses can effectively leverage this alternative to optimize their risk management strategies.

The Benefits of 831(b) Microcaptives

-

Enhanced Risk Management:

Captive insurance under the 831(b) tax code offers businesses a unique opportunity to take control of their risk management strategies. By forming a microcaptive, companies can tailor insurance policies specifically to their industry, operations, and perceived risks. This customization allows businesses to have greater control over coverage, claims, and overall risk mitigation. By managing their own captive insurance, companies can implement proactive risk management techniques and minimize both financial and operational risks. -

Potential Tax Advantages:

One of the primary benefits of utilizing 831(b) microcaptives is the potential for tax advantages. Under this tax code, companies may be eligible for certain tax exemptions, including the ability to exclude a certain portion of the premiums received from their taxable income. This can result in significant tax savings for businesses over time. However, it is important to note that companies must adhere to strict IRS guidelines and proper structuring to fully realize these tax benefits. -

Unleashing Financial Opportunities:

Captive insurance also presents unique financing opportunities for businesses. By forming a microcaptive, companies can generate underwriting profits and invest those funds according to their own risk appetite and business needs. The ability to retain underwriting profits provides businesses with an additional income stream that can be used for various purposes such as funding future claims, expanding operations, or even diversifying their overall investments.

In conclusion, 831(b) microcaptives offer several compelling benefits for businesses seeking alternative insurance solutions. From enhanced risk management and potential tax advantages to the financial opportunities they present, captive insurance allows companies to break free from traditional coverage and embrace a tailored approach to insurance that aligns with their specific needs and objectives.

Navigating the IRS 831(b) Tax Code

Understanding the IRS 831(b) tax code is essential when venturing into the world of captive insurance. This code provides a specific tax designation for small insurance companies, commonly referred to as microcaptives. Operating under this tax code can offer significant advantages and incentives for businesses looking to break free from traditional coverage.

One of the main advantages of utilizing the IRS 831(b) tax code is the potential for reduced taxation. Microcaptives that qualify under this code may be subject to lower tax rates on their insurance premiums and investment income. This presents a key opportunity to optimize the financial benefits of captive insurance, allowing businesses to retain more of their income and allocate it towards growth and risk management efforts.

However, it is crucial to note that strict compliance with the IRS regulations is vital for microcaptives operating under the 831(b) tax code. The Internal Revenue Service has specific guidelines and requirements that must be followed to maintain compliance and uphold the tax advantages offered by this designation. Failing to adhere to these regulations can result in penalties and potentially negate the benefits associated with captive insurance.

Navigating the complexities of the IRS 831(b) tax code requires a comprehensive understanding of the regulations and ongoing adherence to them. Businesses considering venturing into captive insurance should consult with knowledgeable professionals and experts in the field to ensure compliance and maximize the advantages offered by this tax designation.